Receiving an income tax scrutiny notice from the Income Tax Department can be a stressful experience, especially when it's related to an Income Tax Scrutiny Notice. This notice, issued under Section 143(2) of the Income Tax Act, signals that your income tax return (ITR) is being scrutinized for accuracy.

It is part of a process to ensure taxpayers file their returns correctly and pay the right amount of taxes. But what does this notice mean? Why do you receive it, and how should you respond? In this blog, we will break down all the important details about Notice u/s 143(2) to help you navigate this process smoothly.

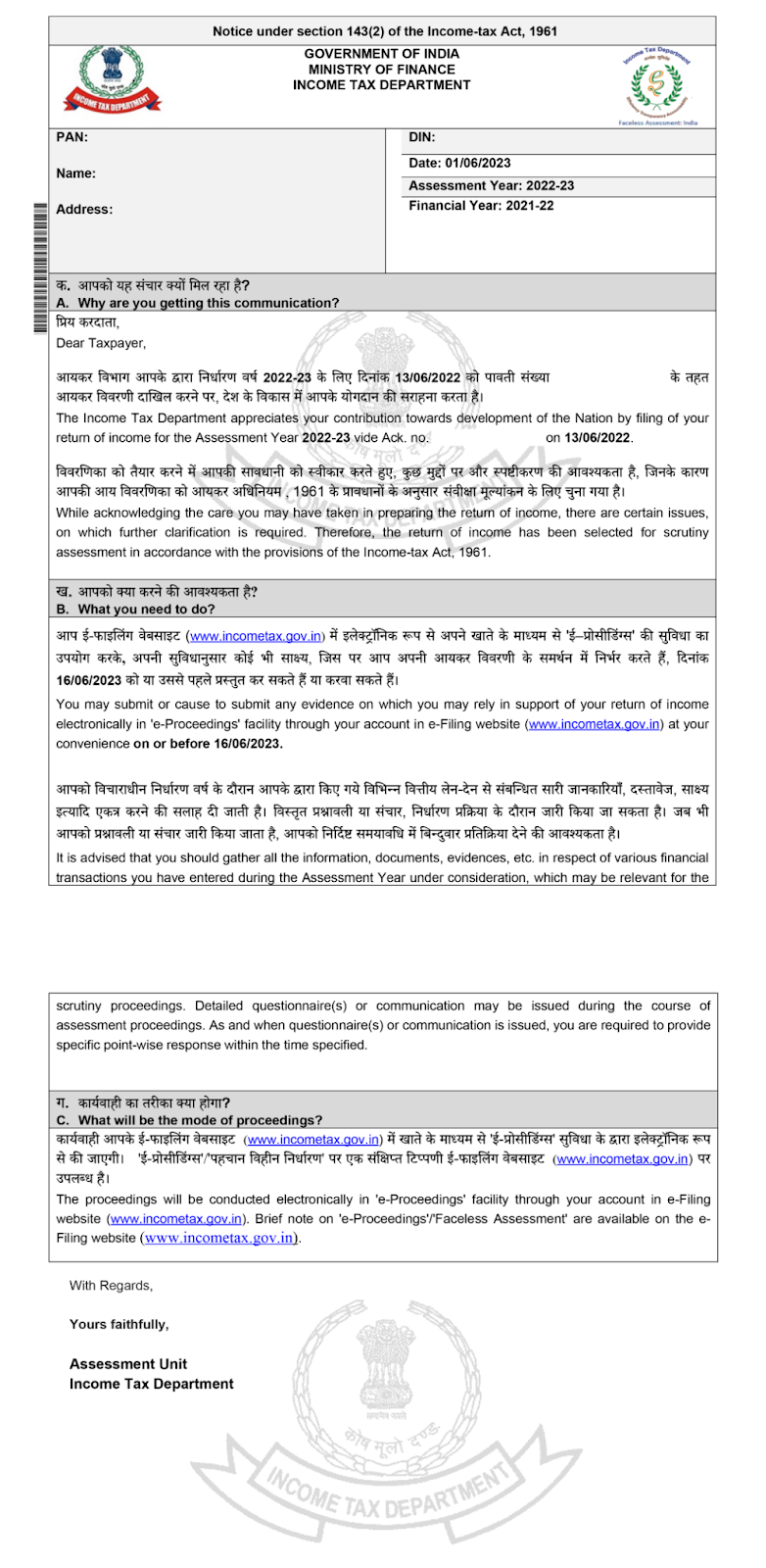

What is Income Tax Scrutiny Notice?

An Income Tax Scrutiny Notice under Section 143(2) is issued when the Income Tax Department selects your income tax return for a detailed scrutiny assessment. This is a more in-depth review than the usual assessment and is done to verify the accuracy and authenticity of the claims you have made in your tax return, such as deductions, exemptions, and reported income. The department conducts this scrutiny to ensure that all the information provided in your ITR is correct and that no errors or fraudulent claims have been made.

The Income Tax Scrutiny Notice under Section 143(2) serves as a preliminary step before the final assessment under Section 143(3). It’s the department’s way of requesting more information or clarification to verify the details provided in your return.

Common Reasons for Receiving an Income Tax Scrutiny Notice

There are several reasons why you might receive an Income tax scrutiny notice under Section 143(2). Some common reasons include:

- Errors in TDS (Tax Deducted at Source): Discrepancies in the TDS details, where the amount deducted by the employer or other parties doesn’t match the amount declared in your return.

- Under-reporting of Income: If the income declared in your return is lower than the income recorded in other documents (like Form 26AS or bank statements), it may trigger a scrutiny.

- Over-reporting of Losses: If you’ve reported more losses than you should have, it may raise red flags.

- Mismatches in Income Figures: This happens when the income declared by you doesn't match the income reported by third parties, such as banks, employers, or other sources.

- Incorrect Claims for Deductions/Exemptions: Incorrect or over-inflated claims for deductions like 80C or exemptions can trigger scrutiny.

- High-Value Transactions: Large transactions such as buying or selling property, making substantial bank deposits, or investments can raise suspicion.

- Defects in the Income Tax Return: If there are any mistakes or missing details in your ITR, the department might issue a notice for further clarification.

- General Clarifications: Sometimes, the department issues a notice to seek general clarification about certain claims or the validity of the return.

Types of Income Tax Scrutiny Notice under Section 143(2)

There are three main types of scrutiny assessments that can be carried out under Section 143(2):

- Limited Scrutiny: This type of scrutiny focuses only on specific areas or discrepancies highlighted in the notice. For example, it might focus on TDS errors or discrepancies in property sale details. Limited scrutiny is often conducted through the Computer-Assisted Scrutiny Selection (CASS) process.

- Complete Scrutiny: This involves a thorough review of the entire ITR, including all claims, deductions, exemptions, and supporting documents. The department will examine all aspects of the return in detail.

- Manual Scrutiny: In this case, cases are selected for scrutiny manually, based on criteria set by the Central Board of Direct Taxes (CBDT). The criteria for selection can vary from year to year.

Time Limit for Issuing Notice u/s 143(2)

The Income Tax Department must issue the income tax scrutiny notice under Section 143(2) within three months from the end of the financial year in which the tax return is filed. For example, if you file your ITR for the financial year 2022-23 by June 2023, the department must issue the notice by 30th June 2024.

This time limit ensures that the department takes prompt action to start the scrutiny process. If the notice is not issued within this time, the return is considered finalized, and the department cannot raise any further questions or demands.

How to Respond to an Income Tax Scrutiny Notice under Section 143(2)?

Receiving an income tax scrutiny notice under Section 143(2) means that you must respond in a timely and accurate manner to avoid any penalties or further scrutiny. Here’s a step-by-step guide to how you should respond:

- Review the Notice: Read the notice carefully to understand the specific issues or discrepancies highlighted by the Income Tax Department. Make a note of the areas where clarification is needed.

- Gather Supporting Documents: Collect all necessary documents, such as bank statements, TDS certificates, income proof, expense receipts, and any other relevant documents, to support your claims in the ITR.

- Draft a Response: Prepare a detailed response to address each point raised by the department. Provide clear explanations for any discrepancies and back up your claims with the relevant documents.

- Submit the Response Online: To submit your response, log in to the Income Tax portal (https://eportal.incometax.gov.in/iec/foservices/#/login). Go to the ‘Pending Actions’ tab and click on the ‘e-Proceedings’ tab. Find the relevant assessment year and click on ‘View Notices/Orders’. You will see the income tax scrutiny notice issued under Section 143(2) and can submit your response by clicking on the ‘Submit Response’ button.

- Keep Track of Further Communications: After submitting your response, the department may issue further notices to seek additional clarifications or documents. Be sure to respond to these promptly.

Time Limit for Final Assessment Order u/s 143(3)

Once the scrutiny is complete and all documents are reviewed, the department will issue a final assessment order under Section 143(3). The department must complete the assessment within a specific time limit, depending on the assessment year (AY):

- For AY 2017-18 or earlier: 21 months from the end of the relevant assessment year.

- For AY 2018-19: 18 months from the end of the relevant assessment year.

- For AY 2019-20 onwards: 12 months from the end of the relevant assessment year.

This timeline allows the department enough time to review the documents, respond to any queries, and finalize the tax liability.

Consequences of Non-Compliance with Notice u/s 143(2)

If you fail to respond to a notice under Section 143(2), there can be serious consequences:

- Penalties: A penalty of up to ₹10,000 may be imposed under Section 272A for each failure to respond to the notice.

- Best Judgment Assessment: If you fail to provide the necessary documents or responses, the Assessing Officer (AO) may carry out a best judgment assessment under Section 144. This means the AO will assess your income and tax liabilities based on available information, potentially resulting in a higher tax demand.

- Legal Consequences: Non-compliance could lead to legal actions, including prosecution. In severe cases, this may involve imprisonment.

Conclusion

An Income Tax Scrutiny Notice may seem intimidating, but with proper understanding and timely compliance, you can address it effectively.

Receiving a notice under Section 143(2) can be intimidating, but it’s important to understand that it’s part of the scrutiny process to ensure the accuracy of your income tax return. If you have filed your return correctly and provided the right documentation, responding to the notice will be a straightforward task. Timely and transparent compliance is key to resolving any issues with the Income Tax Department and avoiding penalties or legal complications.

Remember, the notice serves as a request for clarification, not an accusation of wrongdoing. With the right approach, you can navigate this process without stress and ensure that your tax return is accurately assessed.

FAQ's Related to Income Tax Scrutiny Notice

𝐖𝐡𝐚𝐭 𝐢𝐬 𝐭𝐡𝐞 𝐩𝐮𝐫𝐩𝐨𝐬𝐞 𝐨𝐟 𝐭𝐡𝐞 𝐢𝐧𝐜𝐨𝐦𝐞 𝐭𝐚𝐱 𝐬𝐜𝐫𝐮𝐭𝐢𝐧𝐲 𝐧𝐨𝐭𝐢𝐜𝐞 𝐮𝐧𝐝𝐞𝐫 𝐒𝐞𝐜𝐭𝐢𝐨𝐧 𝟏𝟒𝟑(𝟐)?

The notice under Section 143(2) is issued by the Income Tax Department to inform the taxpayer that their Income Tax Return (ITR) has been selected for a detailed scrutiny assessment. This is to ensure the accuracy of the information provided in the return and verify claims such as deductions, exemptions, and income.

𝐇𝐨𝐰 𝐝𝐨 𝐈 𝐤𝐧𝐨𝐰 𝐢𝐟 𝐈 𝐡𝐚𝐯𝐞 𝐫𝐞𝐜𝐞𝐢𝐯𝐞𝐝 𝐚 𝐍𝐨𝐭𝐢𝐜𝐞 𝐮/𝐬 𝟏𝟒𝟑(𝟐)?

You will receive the notice either by post or through the Income Tax Department's online portal. You can also check your status and any notices issued by logging into the Income Tax e-filing portal (https://incometax.gov.in).

𝐂𝐚𝐧 𝐈 𝐢𝐠𝐧𝐨𝐫𝐞 𝐭𝐡𝐞 𝐢𝐧𝐜𝐨𝐦𝐞 𝐭𝐚𝐱 𝐬𝐜𝐫𝐮𝐭𝐢𝐧𝐲 𝐧𝐨𝐭𝐢𝐜𝐞 𝐮𝐧𝐝𝐞𝐫 𝐒𝐞𝐜𝐭𝐢𝐨𝐧 𝟏𝟒𝟑(𝟐)?

No, you should not ignore the notice. Ignoring the notice can lead to penalties, additional scrutiny, or even legal action. It's essential to respond to the notice within the specified time limit.

𝐖𝐡𝐚𝐭 𝐡𝐚𝐩𝐩𝐞𝐧𝐬 𝐢𝐟 𝐈 𝐦𝐢𝐬𝐬 𝐭𝐡𝐞 𝐝𝐞𝐚𝐝𝐥𝐢𝐧𝐞 𝐭𝐨 𝐫𝐞𝐬𝐩𝐨𝐧𝐝 𝐭𝐨 𝐭𝐡𝐞 𝐧𝐨𝐭𝐢𝐜𝐞?

If you miss the deadline to respond, you may face penalties under Section 272A for non-compliance. The Income Tax Officer (ITO) may also proceed with a best judgment assessment, which may result in higher tax liabilities.

𝐈𝐬 𝐭𝐡𝐞𝐫𝐞 𝐚 𝐩𝐞𝐧𝐚𝐥𝐭𝐲 𝐟𝐨𝐫 𝐫𝐞𝐜𝐞𝐢𝐯𝐢𝐧𝐠 𝐚 𝐧𝐨𝐭𝐢𝐜𝐞 𝐮𝐧𝐝𝐞𝐫 𝐒𝐞𝐜𝐭𝐢𝐨𝐧 𝟏𝟒𝟑(𝟐)?

Receiving the notice itself does not result in any penalty. However, failing to respond to it or failing to provide the necessary documents may attract penalties and interest charges.