Tax-related notifications can often cause confusion, especially when it comes to understanding the notices you may receive from the Income Tax Department. One of the most important notices you might encounter is the Tax Demand Notice issued under Section 156 of the Income Tax Act, 1961.

This tax demand notice serves as a formal demand for payment related to unpaid taxes, penalties, interest, or any other sums determined due by the tax authorities. It is crucial for taxpayers to understand how these notices work, what they entail, and how to respond in order to avoid unnecessary penalties or legal issues.

What Is a Tax Demand Notice Under Section 156?

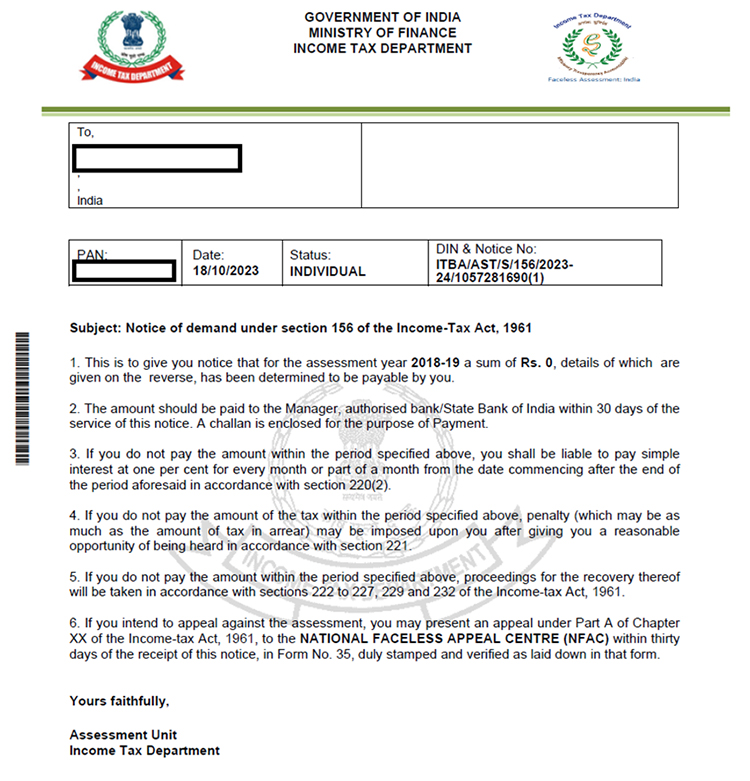

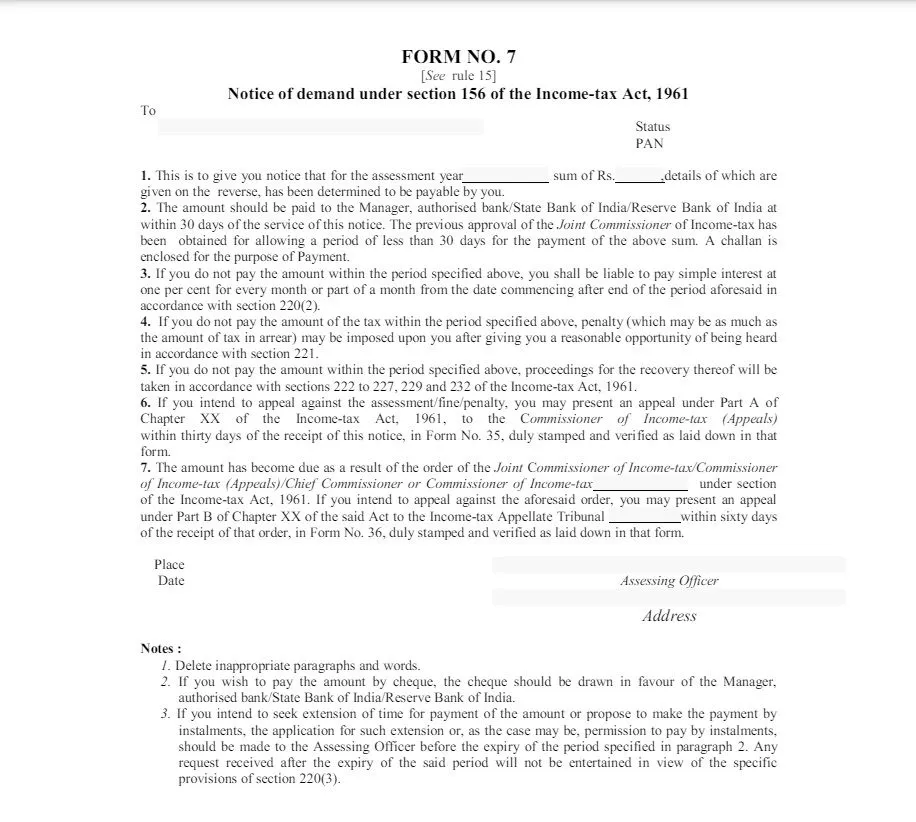

Section 156 of the Income Tax Act is a provision that empowers the Income Tax Department to issue a Tax Demand Notice. The notice informs taxpayers about their outstanding liabilities, which could include tax dues, penalties, interest, or other sums related to the assessment or reassessment of their income.

The notice is typically issued by the Assessing Officer (AO) after an assessment is made, revealing that additional tax is due. These assessments may be triggered by unreported income, incorrect tax calculations, or incomplete information on the taxpayer's part.

Some common situations where such notices are issued include:

- Regular assessment: This happens when the tax authorities assess the returns filed by the taxpayer and find discrepancies or additional amounts due.

- Scrutiny assessment: A more detailed examination of the taxpayer’s financial records.

- Penalty assessment: Under sections like 270A or 271(1)(c), if a penalty is due for underreporting or misreporting income.

- Best judgment assessment: When the Assessing Officer determines the tax liability based on their judgment under Section 144, when the taxpayer fails to cooperate with the authorities.

Key Provisions of Section 156

Section 156 of the Income Tax Act lays down the guidelines for issuing a demand notice. Here’s a breakdown of the key provisions:

- Issuance of a Notice of Demand:

- The Assessing Officer issues a notice of demand in cases where the taxpayer is required to pay any amount of tax, interest, penalty, fine, or any other sum as a result of an order passed under the Income Tax Act.

- If a sum is determined payable under sections 143(1), 200A(1), or 206CB(1), it is considered a notice of demand for the purposes of Section 156.

- Section 156(2) - Special Provisions for Startups:

- For employees of eligible startups who receive sweat equity shares, tax or interest due on such income is payable within 14 days of the earliest of these events:

- 48 months from the end of the relevant assessment year

- The sale of the shares

- The employee ceasing to be with the employer

- For employees of eligible startups who receive sweat equity shares, tax or interest due on such income is payable within 14 days of the earliest of these events:

- Timely Payment:

- The taxpayer is required to settle the amount within 30 days from the date the notice is served. In exceptional cases, the Joint Commissioner of Income Tax may extend or reduce the time limit with prior approval.

How to Respond to a Tax Demand Notice

Once you receive a tax demand notice, it is essential to take prompt action. Ignoring it can lead to interest, penalties, or even legal action. Here's a step-by-step guide on how to respond:

1. Log in to the Income Tax e-Filing Portal

- Use your User ID and Password to access your account on the Income Tax e-filing portal.

2. Select the Option for Responding to the Notice

- Navigate to Pending Actions and select Response to Outstanding Tax Demand.

3. Choose the Appropriate Option

- The portal provides several options for response:

- Demand is Correct: If you agree with the tax demand.

- Demand is Partially Correct: If you agree with some portions of the demand.

- Disagree with Demand: If you contest the entire demand.

- Demand is Not Correct but Agrees to Adjustment: If you acknowledge an error but prefer an adjustment rather than full payment.

Scenarios: How to Respond to the Demand

Scenario 1: Affirming the Accuracy of the Tax Liability (Demand is Correct)

If you agree with the tax demand and are ready to pay:

- Choose Demand is Correct.

- If you have already made the payment, select Yes, Already Paid and provide the Challan Identification Number (CIN), BSR code, serial number, and date of payment.

- If you haven't made the payment, click Not Paid Yet and select Pay Now to proceed to the e-Pay Tax page.

Scenario 2: Disagreeing with the Demand (Demand is Incorrect)

If you do not agree with the tax demand:

- Choose Disagree with Demand.

- Provide the reason for your disagreement. For example:

- Payment has already been made.

- The demand has been reduced by a rectification or appellate order.

- An appeal has been filed, or a rectified return has been submitted.

- Submit your response after filling in the relevant details.

Time Limit to Respond to a Tax Demand Notice

Once you receive a tax demand notice under Section 156, you are required to pay the amount within 30 days from the date of receipt. In some cases, the Assessing Officer can reduce or extend this period with prior approval from the Joint Commissioner. However, it is advisable to act quickly to avoid penalties or interest charges.

If you are unable to pay the entire amount at once, you can apply for an installment plan. This request must be made before the expiration of the 30-day period.

Consequences of Delay in Payment

Failure to respond to a tax demand notice or pay the due amount on time can result in penalties and interest, making the situation more expensive. The key provisions are as follows:

1. Interest on Delayed Payment (Section 220(2))

- Interest is charged at the rate of 1% per month (or part of a month) on the outstanding amount.

- This interest continues to accumulate until the tax is paid, even if an extension or installment plan has been approved.

2. Penalty for Non-Payment (Section 221)

- The Assessing Officer may impose a penalty for failure to pay the tax within the stipulated time.

- The penalty amount can be up to the amount of tax due, and it may increase if the default continues.

- Penalties can be avoided if the taxpayer can prove that the delay was due to reasonable causes.

What Types of Dues are Covered in a Section 156 Notice?

A Section 156 notice can include several types of dues, including:

- Income Tax: If the assessment reveals that additional income tax is due.

- Interest: For delayed payments or other applicable interest charges.

- Penalties: For underreporting income, failing to file returns, or other violations.

- Fines or Other Sums: Any other amounts determined due under the Income Tax Act.

Can Income Tax Demand Be Paid in Installments?

Yes, if you're unable to pay the entire demand at once, you can apply to the Assessing Officer for permission to pay the amount in installments. This application must be submitted before the expiration of the 30-day deadline, and you must provide a valid reason for requesting an installment plan.

For more information please visit:

Income Tax e-Filing Portal – Official portal for responding to notices and filing taxes.

Taxpayer Charter - Government of India – Information on taxpayer rights and obligations.

Section 156 of the Income Tax Act (Bare Act) – Detailed legal provisions.

Understanding Penalties for Non-Compliance – A trusted resource for penalties and legal interpretations.

Conclusion

Understanding and responding to a tax demand notice under Section 156 of the Income Tax Act is essential for every taxpayer. These notices inform you about any outstanding liabilities related to taxes, interest, penalties, or fines, and failing to address them can result in penalties, interest, or even legal consequences. It’s crucial to check the details of the notice carefully, confirm the accuracy of the demand, and take prompt action to pay or contest the demand.

If you agree with the demand, make the payment promptly, and if you disagree, file the appropriate response through the Income Tax e-Filing portal. If necessary, seek professional advice from a tax consultant to navigate the process smoothly and ensure compliance.

By understanding the procedures involved, taxpayers can prevent further complications and maintain a clear record with the Income Tax Department. Always remember to respond within the prescribed time limits, and seek help if you’re uncertain about any details of the demand notice.

FAQ's Related to Tax Demand Notice

𝐖𝐡𝐞𝐧 𝐢𝐬 𝐚 𝐃𝐞𝐦𝐚𝐧𝐝 𝐮/𝐬 𝟏𝟓𝟔 𝐢𝐬𝐬𝐮𝐞𝐝?

It is issued after the completion of an assessment, reassessment, or order by the assessing officer. It specifies the exact amount the taxpayer needs to pay.

𝐖𝐡𝐚𝐭 𝐚𝐫𝐞 𝐭𝐡𝐞 𝐝𝐞𝐭𝐚𝐢𝐥𝐬 𝐦𝐞𝐧𝐭𝐢𝐨𝐧𝐞𝐝 𝐢𝐧 𝐍𝐨𝐭𝐢𝐜𝐞 ?

The notice includes the amount due, the section under which it is levied, and the deadline for payment.

𝐖𝐡𝐚𝐭 𝐡𝐚𝐩𝐩𝐞𝐧𝐬 𝐢𝐟 𝐈 𝐝𝐨𝐧’𝐭 𝐩𝐚𝐲 𝐭𝐡𝐞 𝐚𝐦𝐨𝐮𝐧𝐭 𝐛𝐲 𝐭𝐡𝐞 𝐝𝐮𝐞 𝐝𝐚𝐭𝐞?

Failure to pay by the due date may result in additional penalties and interest.